June 2026 Market Commentary

Hiring Wakes Up, Inflation Heats Up, and the Fed’s Next Move May Be a Hike

The ceasefire with Iran was extended indefinitely back in April, but nobody would mistake the situation for peace. A running “dual blockade” in the Persian Gulf and repeated military flare-ups have kept the truce under strain, and the U.S. launched retaliatory strikes in early June. The administration says a peace agreement is in the works. Investors are not taking that on faith: in a recent Schwab survey, 73% of respondents named geopolitical developments as a top investing concern.

Stocks slid after a strong May jobs report changed the story the market had been telling itself. Good news on hiring turned the spotlight back onto elevated inflation, and expectations for lower interest rates flipped, with markets now pricing in hikes instead. Investors kept taking profits, on the logic that higher borrowing costs will slow the expansion plans of high-growth companies, particularly the AI-heavy semiconductor names.

Meanwhile, the Federal Reserve has a new chairman. Kevin Warsh leads his first FOMC meeting in June, and he arrives with a paper trail: he has argued in recent years that rates could come down, and he has been openly skeptical of the Fed’s habit of steering policy by inflation gauges like CPI and PCE. His term starts at an awkward moment for both positions. Fed governors are staring at a solid labor market on one side and climbing inflation and surging Treasury yields on the other.

Let’s get into the data:

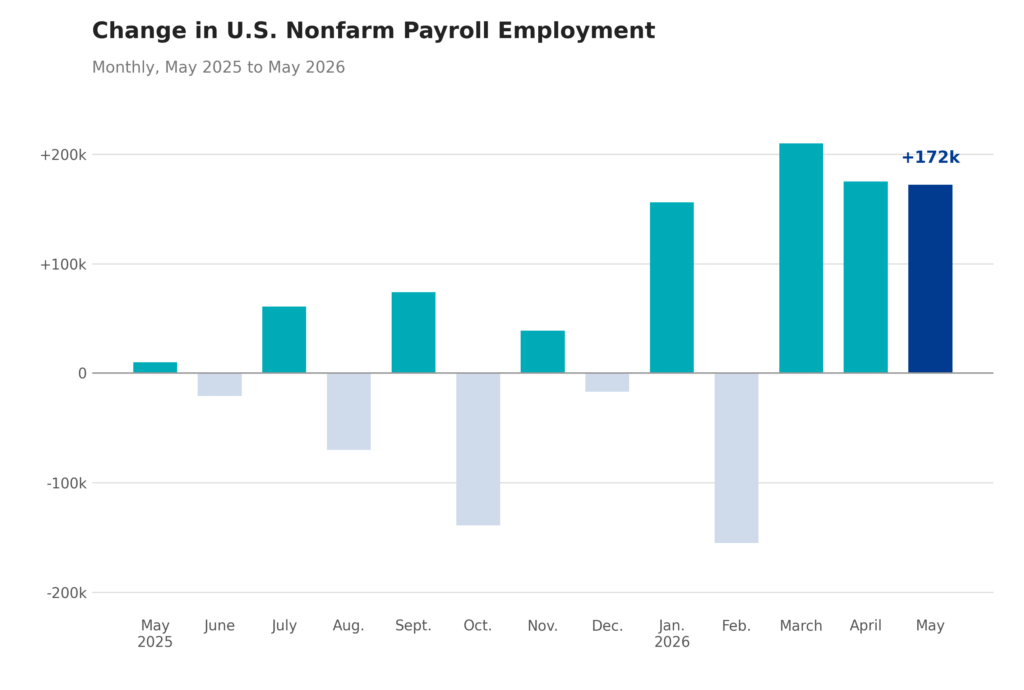

- Non-farm payrolls rose by 172,000. The U.S. Bureau of Labor Statistics (BLS) reported that May blew past the Dow Jones estimate of 80,000 new jobs. The national unemployment rate held at 4.3%.

- Headline CPI rose 4.2% year-over-year. That is the first reading above 4% in three years, although it came in right on expectations.

- Futures markets have priced in at least one quarter-point rate hike before year-end. According to CME FedWatch data, that is a complete reversal from earlier this year, when investors were still hoping for a cut.

- The underlying economy keeps growing. The Atlanta Fed’s GDPNow model tracked Q2 real GDP growth right at 3.7% in its early May updates, a sharp recovery from the sluggish 1.2% Q1 print.

What Does the Data Add Up To?

GDP expectations have bounced back and consumers keep spending. The worry is where the money is coming from. Households are dipping into their reserves to do it: the personal savings rate fell to 2.6%, its lowest level since 2022. Retail CEOs are warning that persistently high fuel prices and food inflation will eventually force a real change in how consumers behave.

The labor market carries its own asterisk. Monthly payroll numbers have stabilized, but inflation has steepened faster than paychecks, so real wage growth is falling behind the cost of living. And because inflation is still climbing, expectations for the path of interest rates have moved dramatically. Many economists now project that rates will not fall again until 2027.

The Fed, for its part, is trying to correct its post-COVID missteps and anchor long-term inflation back to its 2% target. That job keeps getting harder. Fresh structural shocks, including trade tariffs and a regional war choking off energy supply chains, are raising the odds of a prolonged inflationary cycle.

For now, regional Fed leaders are preaching caution rather than panic. San Francisco Fed President Mary Daly noted that while energy and fuel oil shocks are alarming (fuel oil is up 54.3% year-over-year), core goods and broader import prices have not yet bled into worst-case territory. The biggest threat remains the Strait of Hormuz. The longer shipping through the region stays vulnerable, the greater the risk of severe supply chain disruptions downstream.

Which brings everything back to the new chairman. Rates are widely expected to stay put at the June FOMC meeting, so the real event is Warsh’s first press conference, which Wall Street will parse word by word for clues about his communication style and where he wants to take policy.

Chart of the Month: Labor Market

Despite fears that hiring had stalled out, the labor market stabilized over the past three months.

Equity Markets in May

- S&P 500: Rose 0.22%, ending the month at 7,580.06

- Nasdaq Composite: Ended the month at 26,972.62, up 0.2%

- Dow Jones Industrial Average: Finished the month at 51,032.46, up 0.72%

Bond Markets in May

- 10-Year U.S. Treasury Yield: Ended the month at 4.39%, up from 4.30%

- 30-Year U.S. Treasury Yield: Rose to 4.98%, up from 4.88%

- Bloomberg U.S. Aggregate Bond Index: Eked out a barely positive 0.1% return

- Bloomberg Municipal Bond Index: The bright spot for fixed-income investors, gaining 1.15%

The Smart Investor

This is a macroeconomic backdrop to match the summer heat: higher gas prices, elevated headline inflation, and no near-term relief on borrowing costs. Enjoying the season without knocking your long-term plan off course comes down to two things, strategic cash flow planning and portfolio rebalancing.

Budgeting tracks the day-to-day. Cash flow planning is the bigger, forward-looking version: it weighs everything coming in against everything going out, then deliberately routes capital where it does the most good in a high-rate environment, whether that is high-yield savings or paying down expensive debt.

Between a gridlocked war, a brand-new Fed chair, and inflation hanging around like an uninvited guest, the markets are giving everyone whiplash right now. If checking your portfolio makes you sweat a little more than the July sun does, that is a normal reaction, not a character flaw.

You also do not have to white-knuckle these market bumps alone. If your game plan needs adjusting, we are here to help you sort it out and get back to the peace of mind you deserve.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA